|

|

|

| In this edition, we look closer at: |

- The eastern suburbs, hills, and lifestyle property

- Market movement in the southern freeway run down to Baldivis

- A welcome to our new starter in Bunbury

|

| |  |

|

|

|

|

Before looking back to Q4 2022; what may be the main factors surrounding Residential Market Drivers in 2023?

|

|

|

|

|

|

|

|

| |

|

Domestic Tourism

|

|

Domestic Tourism is booming in Western Australia, with the latest Tourism Research Australia figures showing spending hit $1.02 billion recently which is the first time domestic spending has topped $1 billion since early 2019. Over the year, Perth saw 10 million interstate and intrastate visitors spend $9 billion on their trips.

|

| |  |

|

|

|

| As we start the 2023 working year, we wanted to bring you a brief snapshot of the Perth Residential market and this quarter we focus on the eastern suburbs, hills and lifestyle properties with industry specialist Sean Wilson (Perth Executive State Award recipient 2022).

If you would like professional advice on how market changes could effect you personally, please get in touch with Sean via the link below for assistance.

Contact Sean Here |

|

| |

We anticipate the first half of 2023 as one of moderated results whilst the second half as opportunistic, with a positive change in activity if interest rates stabilise and potentially reverse in response to economic shifts.

Notwithstanding, the outlook for the local residential market remains one of the most positive and healthy in Australia for good reason. |

As much as Perth did not experience the highs of the other major capital cities across the country with only modest growth over the past 18 months, on the back of 5 years of falling prices

Mid way 2022 we reached the peak of June 2014 cycle with median prices. On the back of Low stock levels; very low vacancies; eastern states buyers seeing our market as more affordable plus better yields with many buying on the back of yields from outer Perth to regional centres like Bunbury.

Prestige markets western suburbs was first to show signs of coming off earlier in the year while well-appointed family homes demand remained firm. Older houses requiring renovations, vacant land requiring new builds were not necessarily reflecting growth or high demand due to concern around build costs and time frames.

|

Well-appointed family homes, walk in, turnkey and live still attracting good prices in most markets and Land sales continue slowing demand, building approvals continue to ease.

Some issues around Apartments include new supply on the back of build costs, time blow outs, and not being feasible with some off the plans becoming an issue with builders and developers not able to meet the commitments. |

|  |

Perth hasn’t quite reached the heights of larger cities with higher demand of apartment living however noticeable precincts now evolving and will continue to do so around the metro-net stations as well.

However, there are now developing headwinds for the Perth property market including a new round of interest rate rises together with the current high inflation rate / cost of living pressures creating some uncertainty. The official cash rate increasing has slowed demand.

|

| |

Recent data suggests that the growth period nearing two years in the Perth housing market has now come to an end for the foreseeable future, However, with steady population growth and continued low levels of stock we consider the market enters a stabilising period in the last quarter of 2022 to mid-2023 when rate rises are expected to peak; then questions around rates to come back, may trigger another smaller wave of price growth. |

Perth is now one of the most affordable capital cities within Australia with the median house price well below the major capital cites of the eastern states. CoreLogic data shows that in the 12 months to the end of September 2022, Perth house prices grew 4.1% on average. However, dwelling values decreased -0.4% during the September quarter.

The construction industry continues to be impacted by rising labour costs and supply shortages.

This has created more pressure on the established housing stock as many prospective purchasers avoid building in this market.

|

| The Perth rental market is still experiencing strong market conditions with the vacancy rate in September 2022 for the Perth Metropolitan area at 0.7% down from 0.9% during the previous 12 months. The vacancy rate has continued to decline putting upward pressure on rents. A balanced rental market has a vacancy rate generally between 2.5-3.5%, therefore the Perth rental market is still considered to be under supplied. |

|  |

|

|

| |

|

4.1%

|

|

Perth House Prices - 12 Months Prior to end of September 2022

|

|

| |

|

|

| |

|

0.4%

|

|

Dwelling Values - September Quarter

|

|

| |

|

|

| |

|

0.2%

|

|

Rental Vacancy Rate - Previous 12 Months

|

|

| |

|

|---|

|

|

|

|

|

|

|

|

|

| 28% |

| Portion of First Home Buyers |

|

|

|

|---|

|

|

|

Perth Eastern Foothills and Hills

|

|

|

|

Lesmurdie Hill to Perth |

- The Perth foothills market ended with a gradual slow-down from around Sep-Oct 2022 due largely to rising Interest Rates. This is particularly evident in the sub-$600,000 levels with asking prices dropping and lower levels of demand.

Supply still remains limited. There are some examples of buyers having to adjust contract prices down due to financial restrictions. We note quite a few rental property / investor led property being sold as the owners are able to realise what they want or need for the property. This is putting pressure on the rental market and stock levels.

Some early signs of investors moving back into the Perth foothills market following an extended period of inactivity.

|

- Whereas the Hills lifestyle market ended strongly with little signs of slow down. This was particularly apparent in the $1.50m plus market with strong activity for unique property ranging in price right up to $4.00m level.

We have seen multiple sales across the City of Kalamunda, Shire of Mundaring and parts of City of Swan at the $2.20m to low $4.00m’s, including some property that have never before sold. Some increased activity around the Swan Valley / Swan River area.

|

Greenmount Hill Great Eastern Highway |

Mohogany Creek Inn |

- Notable sales: multiple sales in Darlington, Glen Forrest and Gooseberry Hill from $2.20m to $3.70m. Multiple sales activity in Helena Valley, Kalamunda, Lesmurdie and Bickley from $1.50m to $2.60m.

We also note a prominent lifestyle property featured on the most recent series of Grand Designs Australia. The dwelling is not yet completed but when finished, will comprise one of the most unique, interesting homes in the Perth Eastern Hills.

Also multiple large unique new builds all across the Perth Hills with Architects busy on new projects.

|

|

|

Let's Turn Our Attention South...

|

|

|

|

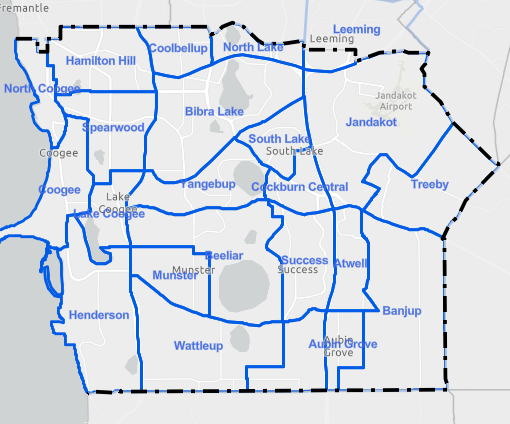

The market in the City of Cockburn is still firm and with continued capital and rental growth over the past 12 months. Suburbs of Success: +5.5%, Atwell: +11.6%, Aubin Grove: +1.9%, Beeliar: +10.1 % and Cockburn Central: +13.2% over this period. There is still limited good stock and an excess of local and interstate buyers has kept the time on market for established housing at 15 days and strata properties at 37 days. Despite recent interest rate rises, the southern corridor remains buoyant, given the market price segment is for first home buyers and investors alike.

|

|

|

Sales of Interest - Baldivis

|

|

|

| Date |

Previous Sale Price |

Date |

Sale Price |

Increase |

Year Difference |

Age |

Land Size |

Living Area |

| Jun-19 |

$395,000 |

May-22 |

$615,000 |

55.7% |

2.99 |

2015 |

601 |

237 |

| Comments: Comprises of a 4 bed, 2 bath home with a standard fit-out. No major improvements to the dwelling between sales representing a 55.7% increase in value. |

|

| 245 Eighty Road Baldivis | |  |

|

|

| Date |

Previous Sale Price |

Date |

Sale Price |

Increase |

Year Difference |

Age |

Land Size |

Living Area |

| Jul-20 |

$599,000 |

Oct-22 |

$850,000 |

41.9% |

2.28 |

2005 |

4005 |

235 |

Comments: Comprises of a 5 bed, 3 bath two storey home with a renovated fit-out. Full internal establishment of floor coverings, kitchen, bathrooms and window treatments of dwelling between sales representing a 41.9% increase in value. |

|

| 25 St James Drive Baldivis | | |

|

|

| Date |

Previous Sale Price |

Date |

Sale Price |

Increase |

Year Difference |

Age |

Land Size |

Living Area |

| Jun-21 |

$560,000 |

Nov-22 |

$650,000 |

16.1% |

1.45 |

2017 |

529 |

242 |

Comments: Comprises a circa 2017 built two storey residential dwelling. Accommodates 4 bed, 2 bath. Standard fit-out. No major improvements to the dwelling between sales representing a 16.1% increase in value. |

|

|

| |

| Please Welcome Our Latest Addition To The Team |

Rex Stafford |

With over 40 years' experience in the real estate valuation industry he has undertaken valuations of most types of real estate asset classes both freehold and leasehold in all the mainland states of Australia.

Rex commenced his career as a valuer with the Commonwealth Bank in Perth before moving into private industry in 1989 in Sydney where he worked for a number different major valuation companies one of which he partly owned and has acted as an expert witness in court and served on the Professional Interview panel of the NSW Division of the API.

Over the last decade Rex has specialised in the valuation of residential properties and small rural holdings in regional Western Australia. He joins us valuing property in the Bunbury and South West region. |

|

|

|

|

|

|

|

Click here to unsubscribe.

CBRE: Level 25 QV1 Building 250 St Georges Terrace, Perth WA 6000 Australia This communication is from CBRE or one of its associated/subsidiary companies. This communication contains information which is confidential and may be privileged. If you are not the intended recipient, please contact the sender immediately. Any use of its contents is strictly prohibited and you must not copy, send or disclose it, or rely on its contents in any way whatsoever. CBRE collects, holds, uses and discloses personal information in accordance with our Privacy Policy which can be viewed here. Information herein has been obtained from sources believed reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the market. Reasonable care has been taken to ensure that this communication (and any attachments or hyperlinks contained within it) is free from computer viruses. No responsibility is accepted by CBRE Pty Ltd or its associated/subsidiary companies and the recipient should carry out any appropriate virus checks.

Address: Level 25 QV1 Building 250 St Georges Terrace Perth WA 6000 Australia

|

|

|