|

Quietly, and far from the headlines, the suburban office market continues to strengthen.

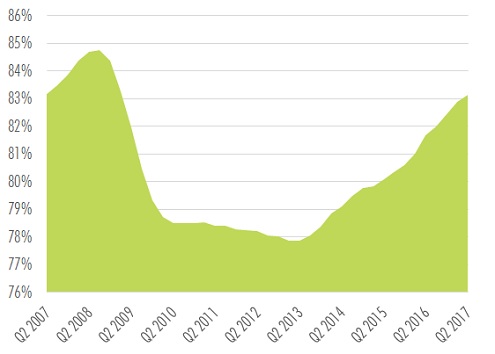

In Q2 2017, the office market in the four suburban Philadelphia counties in Pennsylvania achieved their sixth consecutive quarter of positive net absorption - the longest streak since 2008. Occupancy has been rising in an upward trajectory for over four years. The average asking rent for space, which has plateaued over the past year, is at its highest level since 2009. Key to these strengthening fundamentals has been the lack of any significant, new projects. |

| XXXX |

| Figure 1: Suburban Philadelphia Office Occupancy* |

|

| *4-quarter rolling average of office occupancy (Source: CBRE Research) |

| X |

But it isn't rosy everywhere. Figure 2 shows some of the variation.

On the more positive side, the Main Line continues to be extremely tight for space options, and the bellwether submarket of King of Prussia/Valley Forge has seen occupancy rise for seven consecutive quarters. Meanwhile, the Exton/West Chester submarket has realized a drop in its vacancy rate of 23.8% three years ago to 13.9% in Q2 2017.

Though suffering from higher vacancy, Bucks County has shown considerable improvement recently (see Lower and Central Bucks below). Even Horsham and Fort Washington have driven occupancy higher, compared to last year. Blue Bell as well shouldn't be overlooked, having made some material gains in occupancy.

On the other hand, softer demand for space has been realized over the past year in Bala, Conshohocken, Delaware County, and Plymouth Meeting. These are relatively tight markets for space, though, and nothing alarming seems at play at this point. In a less favorable spot are the Upper Main Line and Jenkintown submarkets, which have seen positive absorption in 2017, but still wrestle with high vacancy and overall flat demand since mid-2016. |

| X |

Figure 2: Suburban PA Office Submarkets

(Occupancy Rate vs. Occupancy Gains) |

|

| (Source: CBRE Research) |

| X |

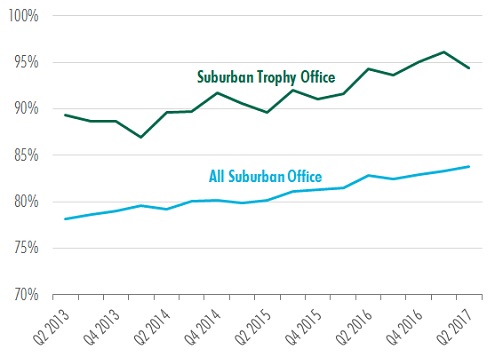

| The market for trophy office space in the suburbs, near its highest occupancy levels tracked, had a tough quarter, though. Over 114,000 of negative absorption occurred, dropping the occupancy rate for suburban trophy offices slightly to 94.4%. Over the last year, demand has essentially been flat. Nonetheless, asking rents in Q2 2017 reached their highest levels ($35.07 per sq. ft.) this cycle, and occupancy continues to trend upwards. |

| X |

| Figure 3: Suburban Trophy Office Occupancy |

|

| (Source: CBRE Research) |

| X |

Contact:

Ian Anderson

Director of Research and Analysis

T + 1 215 561 8997

ian.anderson2@cbre.com |

| |

|

|

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330).

Please consider the environment before printing this email.

CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166.

Address: Two Liberty Place, 50 S. 16th Street, Suite 3000 Suite 700, Philadelphia PA 19102

© 2026 CBRE Statistics contained herein may represent a different data set than that used to generate National Vacancy and Availability Index statistics published by CBRE Corporate Communications or CBRE's research and econometric forecasting unit, CBRE Econometric Advisors. Information herein has been obtained from sources believed reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to independently confirm its accuracy and completeness. Any projections, opinions, assumptions or estimates used are for example only and do not represent the current or future performance of the market. This information is designed exclusively for use by CBRE clients, and cannot be reproduced without prior written permission of CBRE.

CBRE and the CBRE logo are service marks of CBRE, Inc. and/or its affiliated or related companies in the United States and other countries. All other marks displayed on this document are the property of their respective owners.

Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

|