|

|

|

CBRE has published the fourth quarter 2021 Salt Lake-Provo office market report. What is the current state of the office market? Since the black swan event occurred in March 2019, the media has repeatedly reported the death of the office. Is the office market dead? Is office evolving? I will let you come to your own conclusions based on market data instead of anecdotal stories. Let's get started.

|

|

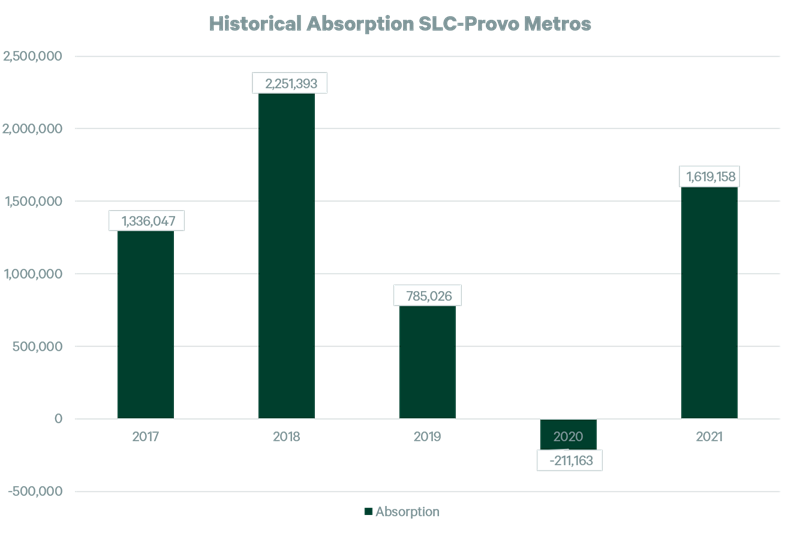

Net absorption is a good indicator of a healthy market. For the past five years, including the last two years of the historical 10 plus years of an extraordinary economic growth cycle, positive absorption was between 1.3 and 2.3+ MSF. It dropped significantly when the cataclysmic event occurred, and the economy shut down. As we have been working through the pandemic for the past two years, net absorption has begun to come back, reaching over 1.6 MSF and representing 73% of absorption reported in 2018. We are still working our way through the uncertain, bumpy road of COVID, but positive net absorption came back in a big way.

|

|

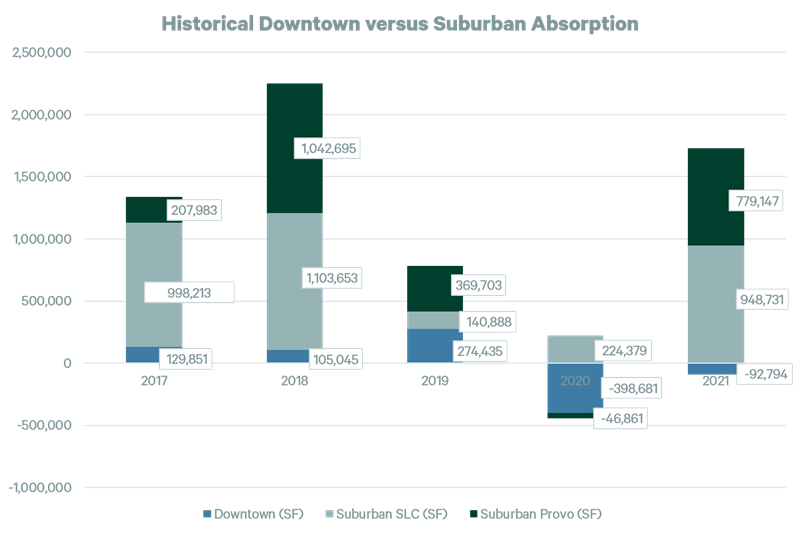

While overall net absorption is strong in the Salt Lake Provo metros, is there a significant difference between downtown and suburban markets? Historically the suburban market has outpaced downtown, and this trend is still occurring.

|

|

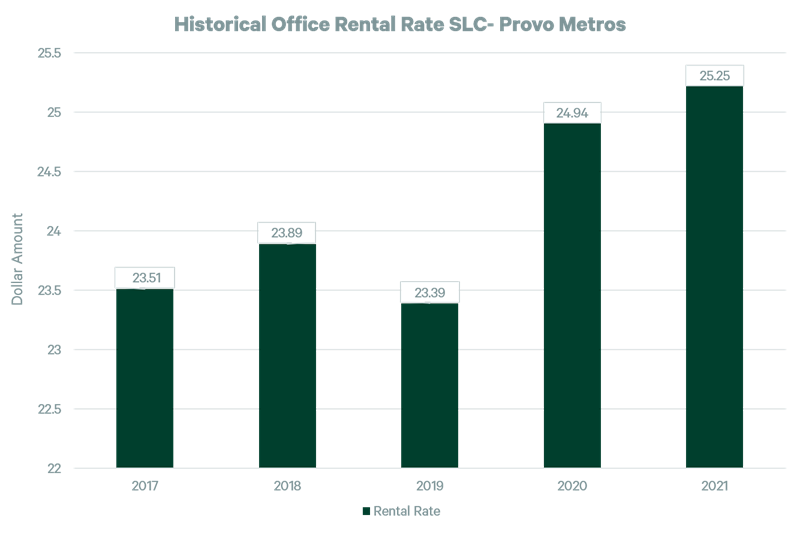

Rental rate growth stimulates office investment. Let's consider what has happened over the past five years. Have rents increased or declined?

|

|

Even with the pandemic, rental rates have increased, as new Class A buildings have delivered and driven rates up. In addition, the more recent inflationary pressure on materials, energy, and labor costs have also affected rental rates.

|

|

Vacancy also indicates a market's strength. What has the past five years shown?

|

|

Vacancy increased in 2020 due to the number of new buildings delivered to the office market. In 2020, 2.5MSF was delivered and in 2021 1.9MSF was supplied. About 1.3MSF is still under construction, but few are speculative buildings. Most of the newly constructed buildings have been 70% leased at the time the building receives a certificate of occupancy.

|

|

Lease activity has remained strong throughout the Salt Lake and Provo Metros, with more tenants executing long-term commitments for big blocks of spaces. New company entrants, in-migration, and expansions are occurring in the market, including Metrodora Institute executing an 11-year, 54,000 sq. ft. lease in Farirbourne Station Office; Byte leasing approximately 60,000 SF in Thanksgiving Park Building 5; HCA MountainStar’s divisional office expanding their footprint from one floor to two floors at the World Trade Center; Xenter taking 30,000 sq. ft. in the Irvine Office Park in Draper; and the expansion of Recursion Pharmaceuticals and entry of Denali Therapeutics in downtown Salt Lake City, Each taking approximately 50,000 sq. ft. in Phase II of SLC Industry.

|

|

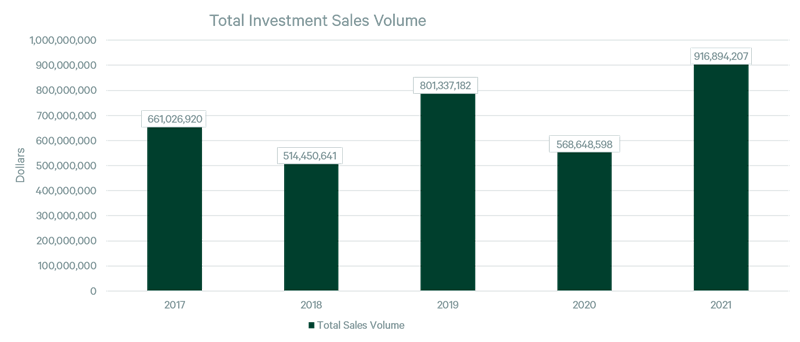

Are investors buying office buildings? If the office is declining would there be buyers purchasing buildings at cap rates achieved during the previous 10+ year growth period? Sales volume increased in 2021 and exceeded the volume during the pre-pandemic.

|

Notable sales included:

- Vista Station in Draper

- Lake Pointe Corporate Center in West Valley

- CHG in the View at 72

- Ancestry buildings in Lehi

- 136 Center buildings in Draper

- The Felt Building in downtown SLC

- The Entrata building in Lehi, and Jordan Valley Tech Center in South Jordan.

Robust sales activity is a good sign, with more institutional buyers purchasing office buildings in the local market and local developers accruing profits. Cap rates have remained stable even with the uncertainty of the pandemic, as shown in the figure below. |

|

CAP Rates (Office CBD)

|

|

Class

|

Lower Limit

|

Upper Limit

|

|---|

|

A

|

5.00%

|

7.00%

| |

B

|

6.50%

|

8.00%

|

|

|

|

|

CAP Rates (Office Suburban)

|

|

Class

|

Lower Limit

|

Upper Limit

|

|---|

|

A

|

5.75%

|

7.00%

| |

B

|

6.50%

|

7.75%

|

|

|

|

|

The flight to quality continues and has accelerated since the beginning of the pandemic. Now that we have shown that we can work anywhere, there needs to be another reason to come to the office. The office must serve a purpose and be meaningful. Does the office attract employee collaboration, efficiency, and promote innovation? Does the building provide amenities, outdoor space, HVAC systems that provide a healthy and safe environment, building meeting rooms, and café and lounge areas? Corporations have increased spend to lease this type of space, since talent retention and attraction have a far greater impact than occupancy costs.

With Class A vacancy lower than Class B, many landlords have included these amenities in new construction. Landlords of existing Class A buildings are spending millions on upgrades. Some examples include the World Trade Center, Kearns Building, Gateway Tower West, 515 Tower, 250 Tower, and Salt Lake Industry's re-adaptive use of warehouse space which is over 95% leased.

With this historical overview, is the office dead? I'll let you answer that question yourself.

|

|

We look forward to your questions, please email or call us. We look forward to serving you in 2022.

|

|

|

|

|

Unsubscribe

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330). Please consider the environment before printing this email. CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166. Address: 222 South Main Street, 4th Floor Suite 700, Salt Lake City UT 84101

THIS IS A MARKETING COMMUNICATION © 2025 CBRE, Inc. All rights reserved. This information has been obtained from sources believed reliable, but has not been verified for accuracy or completeness. You should conduct a careful, independent investigation of the property and verify all information. Any reliance on this information is solely at your own risk. CBRE and the CBRE logo are service marks of CBRE, Inc. All other marks displayed on this document are the property of their respective owners, and the use of such logos does not imply any affiliation with or endorsement of CBRE. Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

All of CBRE's COVID-19 related materials have been developed with information from the World Health Organization, the Centers for Disease Control & Prevention (and similar global organizations), public health experts, industrial hygienists, and global subject matter experts across CBRE and our strategic suppliers. Our materials may not be suitable for application to all facilities or situations.

Ultimately, occupiers and landlords must make and implement their own reopening decisions for their individual stakeholders and facilities. CBRE's guidance is intended to help facilitate those discussions and expedite the implementation of those decisions once made by the client. We make no representations or warranties regarding the accuracy or completeness of these materials. CBRE cannot ensure safety and disclaims all liability arising from use of these materials.

|

|

|