|

|

| Where do we go from here? |

“I am not sure what the next few quarters hold, but I am excited about the next few years.” Tyler, Keiffer and I spent a few days in Boston and New York meeting with developers, operators and capital and this quote might have summed up the overall sentiment.

Blackstone offered a similar thesis on their second-quarter earnings conference call saying: For real estate, “the good news is it’s all about a question of when and not if it will recover." Continuing to say, “The building blocks for this recovery are clearly coming into place,” adding that in the broad economy including real estate the “dealmaking pause is behind us."

While the short term is still unclear CBRE has also been seeing some encouraging green shoots in both the leasing fundamentals and the capital markets.

Leasing Fundamentals

On the fundamentals side it is evident across the country that construction has slowed, so the key is demand. With a laser focus here, we were pleasantly surprised to learn that leasing activity finished the first half of 2025 on a high note including the most leasing for a June on record. (Yes! The largest leasing CBRE has ever recorded in June!) YTD leasing finished mid-year at 424 million sq. ft., 8.5% higher than this time last year. Not sure anyone was predicting a record June, but this was likely bolstered by a hangover from the pause we saw in April and May. That being said, it is very encouraging to see this strong month and an overall strong first half of 2025. CBRE does not count leasing as absorption until the Tenant occupies, so much of this leasing will not show up in the statistics for 90-120 days.

Denver continues to hover in the mid-high 7% direct vacancy range dropping in Q424, rising slightly in Q125 and then dropping again this last quarter. That being said we are optimistic for two reasons.

- Construction is at cyclical lows and has been there for some time; nearly two years ahead of the rest of the country - The construction pipeline saw a decrease as only 462,000 sq. ft. broke ground and 662,000 sq. ft. delivered in Q2.

- Sub-Leasing, a harbinger of vacancy has stayed low - sublease availability remains low at 1.2% of the market despite battery manufacturer Amprius listing for sublease their 800K SF space on I76 having never occupied the space after signing in Q1 2024.

That explains supply, but what is driving leasing demand?

- Flight to Quality and Smaller Spaces. In Denver, buildings-built pre-2000 have seen a 270 bps increase in vacancy compared to less than 1% for the overall market. That being said, small spaces of any vintage continue to thrive. When separated by size, the market is consistently tighter the smaller they get.

- Early Renewals. 34% of 2025 leasing are renewals nationally. We are also seeing higher rates on renewals as landlords have leverage due to Tenant hesitancy to move.

- 3PL outsourcing. Retailers/wholesalers are outsourcing to 3PLs to gain flexibility, illustrating demand but uncertainty.

- Manufacturing. While 3PLs remained the most active occupier, we also saw significant increase in Manufacturing demand, with leasing up 51% compared with last year.

Capital Markets

On the capital markets side of industrial there is strong appetite for the “right” deals. We have seen almost zero closing volatility from Q2 tariff related headlines and liquidity has improved for equity and debt creating a competitive environment. Capital raising continues to be difficult for institutional investors, but based on our meetings, groups are getting to their goals, maybe just more slowly than they would like.

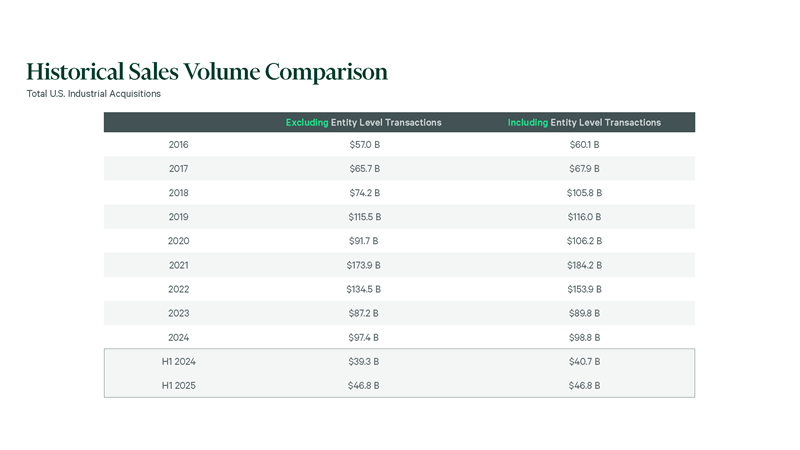

Industrial sales volume in H1 2025 Nationally topped H1 2024 by 16% recording $46.8B in industrial sales and Denver saw a significant increase as well with $717 million in Q2 sales volume. This marked the highest quarterly total in Denver since Q2 2022 jumping 113.8% compared to the $335 million that transacted in Q2 2024. In Salt Lake City our team has closed $330 million of industrial sales in the last three quarters highlighting Salt Lake City as one of the most sought after industrial markets in the country.

While investors are focused on industrial leasing fundamentals, part of what is making the capital markets click is that industrial Debt is more abundant than it has been since interest rates began to rise in 2022 providing buyers with more options despite continued somewhat elevated interest rates. Life Insurance Companies, Bank’s, CMBS, and Debt Funds are all active today.

Overall, both Buyers and Sellers are seeing this as a moment to execute and from our standpoint for good reason.

We are excited about the future and feel like industrial has a wind at our back.

Our biggest compliment is to be asked to be an advisor and partner in helping our clients execute their goals. Please let us know how we can help build a case for your business plan.

|

|

Top Q2 2025 Leases

|

|

Tenant

|

Industry

|

Sq. Ft.

|

Submarket

|

Type

|

|---|

|

National Tire Wholesale

|

Transportation & Distribution

|

264,431

|

Airport

|

New

| |

360Pack

|

Goods MFG

|

110,000

|

Airport

|

Renewal

| |

Chadwell Supply

|

Building Materials & Construction MFG

|

103,922

|

Airport

|

New

| |

RMS Cranes

|

Other

|

98,730

|

I-76 Corridor

|

New

| |

Pack-Rat

|

Transportation & Distribution

|

94,000

|

Airport

|

Renewal

|

|

|

|

|

Q2 brought two (2) investment sales closings in Parc Santa Fe and Arapahoe Business Park I & II & 345 Inverness. Parc Santa Fe, located in Denver’s Southwest submarket is 100% occupied to eight (8) tenants including Terumo, who anchors the project and has a long term remaining. This Class A project features heavy power, easy accessibility to US 85 and 470. Arapahoe Business Park I & II and 345 Inverness is a 10-building industrial/flex Portfolio located in the constrained Southeast submarket and the Portfolio experienced significant leasing momentum up to close to round it out at 98% leased. These buildings cater to tenants in the market looking for industrial flex space while being surrounded by various major thoroughfares, a highly educated workforce and are enhanced by the proximity to Centennial Airport, which 345 Inverness sits adjacent to.

25 Commerce Park – a newly delivered Class A, three (3) building portfolio that sits adjacent to the I-25 and E-470 interchange in Thornton, CO - is currently taking bids. The project is already 71% leased to three (3) tenants with 12.81 WALT Remaining while the remaining vacancy of Building 1 is divisible down to 22,000 SF offering lease-up flexibility and particularity given the various tenant requirements in the market today.

Looking forward, preparations for four other deals are underway so be sure to look out for those in the coming weeks!

|

|

| 25 Commerce Park |

|  |

|

|

|

NEOTech Building

(5800 Kennedy) |

|

|

|

|---|

|

|

|

| Upland Distribution Portfolio & Denver Business Center |

| |

|

|

| Raceway Commerce Center |

| |

|

|

| Potomac Park I & II |

|

|

|---|

|

|

| 1250 Zuni |

| |

|

|

| I-76 & 96th Industrial Opportunity |

| |

|

|

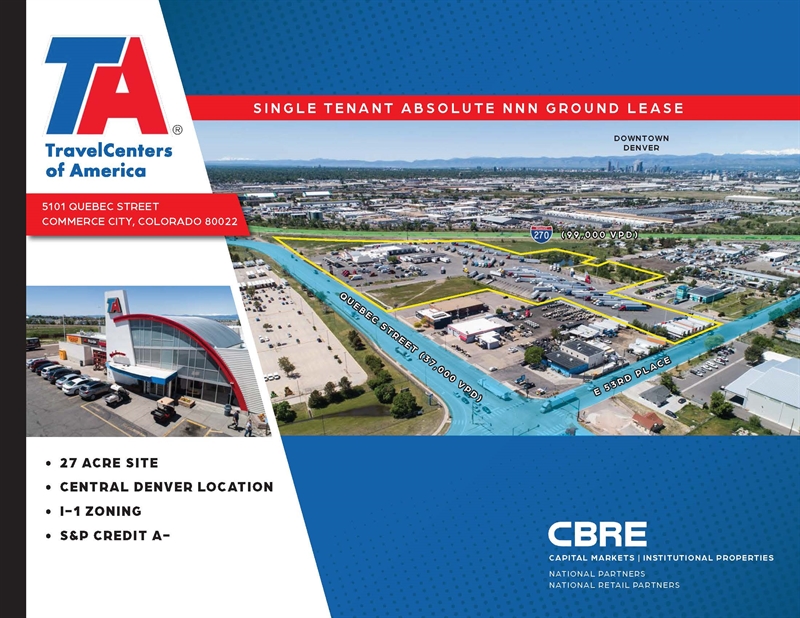

| 5101 Quebec Street |

|

|

|---|

|

|

|

| Arapahoe Business Park I & II & 345 Inverness |

| |

|

|

| Parc Santa Fe |

|

|

|---|

|

|

|

| Please join us in welcoming Brynn Touchstone to the Denver team! Originally hailing from the sunny shores of Santa Rosa, Florida, Brynn brings a fresh perspective and a keen analytical mind to our underwriting team. When she's not crunching numbers, Brynn enjoys exploring the great outdoors, with a passion for hiking, mountain biking, and hitting the slopes. Brynn will be diving right in, focusing on underwriting financials for our investment sales deals, and we're excited to see the contributions Brynn will make and look forward to introducing her to our clients! |

| |  |

|

|

|

|

|

|

|

Unsubscribe

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330). Please consider the environment before printing this email. CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166. Address: 2100 McKinney Ave Suite 700, Dallas TX 75201

THIS IS A MARKETING COMMUNICATION © 2026 CBRE, Inc. All rights reserved. This information has been obtained from sources believed reliable but has not been verified for accuracy or completeness. CBRE, Inc. makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy, completeness, or reliability of the information contained herein. You should conduct a careful, independent investigation of the property and verify all information. Any reliance on this information is solely at your own risk. CBRE and the CBRE logo are service marks of CBRE, Inc. All other marks displayed on this document are the property of their respective owners, and the use of such logos does not imply any affiliation with or endorsement of CBRE. Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

|

|