|

|

Francis | Ybarra | Moothart | Birrell | Santangelo | Korinek | Britt | Coleman | Grabher | Thorp | Post |

|

State of the Commercial Real Estate Debt Market

|

|

- How cuts could impact adjustable and fixed interest rates: The Federal Reserve’s interest rate cuts directly influence adjustable-rate mortgages tied to short-term rates like SOFR or Prime. However, fixed interest rates incorporate expectations of future Fed actions, the long-term economic outlook, and inflation forecasts, rather than just the outcomes of the next FOMC meeting. While the Fed’s decisions don’t directly impact fixed rates, which are based on long-term inflation expectations, economic indicators such as consumer spending and employment reports are more likely to affect these medium- to long-term fixed rates than Fed rate cuts.

- Rates Declining: The decline in interest rates has positively impacted lending activity, particularly for multi-family and industrial properties, which remain highly favored. Retail properties are also seeing renewed interest, expanding beyond traditional grocery-anchored centers with an increase in demand for strip, neighborhood, and regional power centers. Debt for office continues to be challenged with those lenders willing to lend on the asset class preferring Class A, stabilized properties with strong credit tenants, best-in-class sponsors, and a diversified rent roll.

|

- Maturity Wall and Refinancing Challenges: A significant portion of CRE debt, approximately $1.7 trillion, is set to mature between 2024 and year end 2025. This “maturity wall” presents a substantial challenge, as most loans will be repriced at higher interest rates creating significant cash infusion requirements for borrowers. The ability for borrowers to navigate this period will be crucial in determining the market’s stability.

|

- Operational and Construction Costs: Operational costs for commercial real estate have been rising due to increased labor costs, higher maintenance and utility expenses, and elevated insurance premiums driven by inflation and natural disasters. To counter these rising costs, many operators are investing in smart building technologies and data analytics to optimize efficiency. On the construction side, costs have surged due to material price hikes, labor shortages, regulatory compliance, and higher financing costs. Despite these challenges, there are signs of stabilization in material prices and potential cost control through innovative construction methods. Overall, while costs remain high, technology and efficiency investments are helping to mitigate some of these pressures.

|

- Capital Availability and Cost of Capital: Despite market uncertainties, there is a prevailing optimistic lending outlook heading into 2025. Most life company lenders still have allocations for this year. And, starting in October, most lenders will begin offering loan quotes for 2025 production. Capital sources remain predominantly cautious, with conservative leverage and thoroughly underwritten offerings. A common theme among many lenders is the desire to seek higher-yielding opportunities and they are willing to consider more “outside-the-box” deals to deploy these funds. Life insurance company construction loan programs may offer higher initial loan proceeds and provide permanent loan terms of 7 years and beyond with a slight premium in spread.

|

- Opportunity in CRE: While there is cause for concern heading into the second half of 2024, most CRE sectors will be supported by a constructive economic backdrop, suggesting that the market is over-pricing the risks and, in turn, setting up an opportunity for investors to take advantage of attractive valuations in CRE.

|

|

|

Current Index Rates and Trends

|

|

The below matrix compares key index rates over the last 12 months as of 10/1/2024. The US Treasury yield curve is no longer inverted, indicating investor sentiment no longer assumes a pending recessionary period. |

|

INDEX

|

AS OF 10/1/24

|

AS OF 7/2/24

|

AS OF 10/2/23

|

12-MO. CHANGE

|

|---|

|

10-YR US Treasury

|

3.74%

|

4.44%

|

4.69%

|

-0.95%

| |

7-YR US Treasury

|

3.60%

|

4.40%

|

4.73%

|

-1.13%

| |

5-YR US Treasury

|

3.52%

|

4.40%

|

4.71%

|

-1.19%

| |

3-YR US Treasury

|

3.52%

|

4.56%

|

4.89%

|

-1.37%

| |

6-MO US Treasury

|

4.37%

|

5.31%

|

5.55%

|

-1.18%

| |

*SOFR-NY FED-30-DAY TERM

|

5.05%

|

5.35%

|

5.32%

|

-0.27%

|

|

|

|

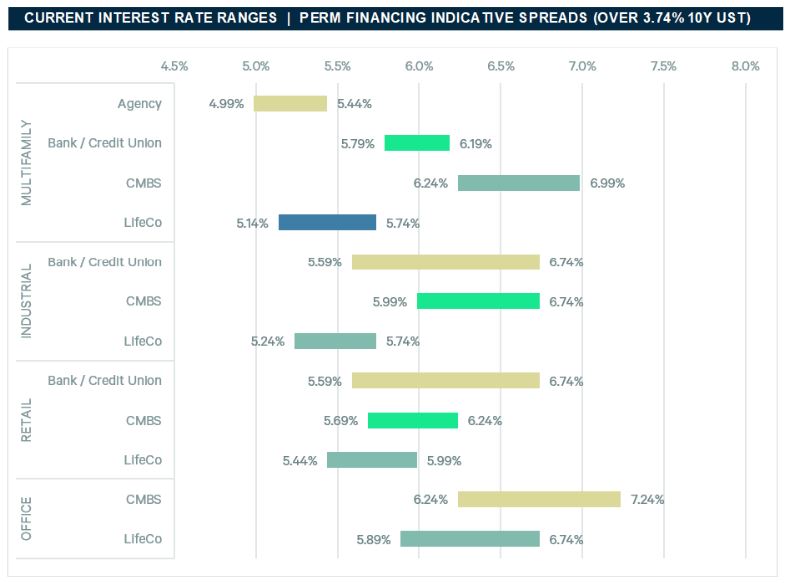

The below matrix compares fixed rate permanent financing pricing by property and lender type as of 10/1/2024, based on an assumed 10-year UST index rate of 3.74%. Please reach out to a producer for specific deal terms.

|

|

Source: CBRE Debt & Structured Finance recently quoted deals (Agency pricing represents conventional-sized deals at $7.5M+).

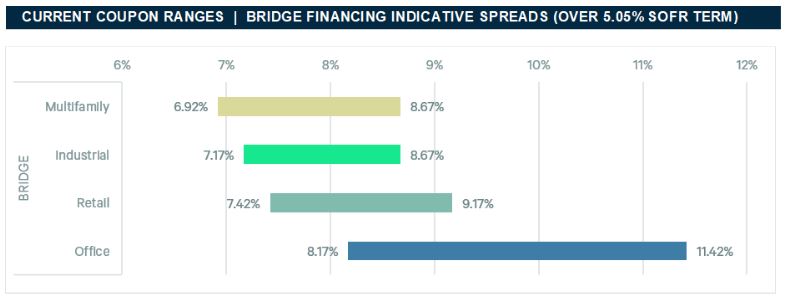

The below matrix compares floating rate bridge financing pricing by property type as of 10/1/2024, based on an assumed 30-Day Term SOFR index rate of 5.05%. Please reach out to a producer for specific deal terms.

|

Source: CBRE Debt & Structured Finance recently quoted deal |

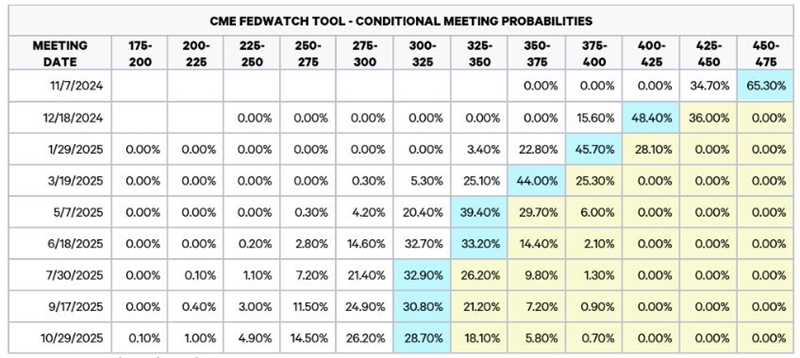

| FEDERAL FUNDS RATE CUT PROBABILITY |

The below chart tracks the probabilities of changes to the Fed target rate and U.S. monetary policy according to interest rate traders, as implied by 30-Day Fed Funds futures pricing data.

|

Fed Makes First of Several Expected Rate Cuts

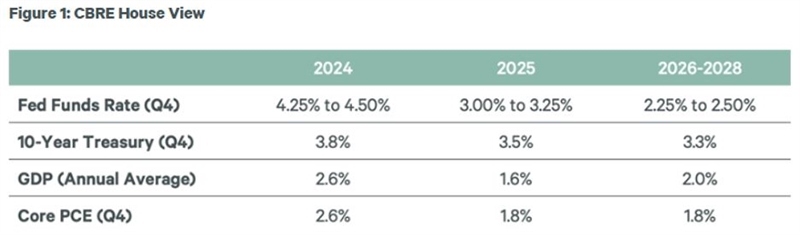

The Fed indicated that it expects an additional 50 bps in cuts this year and 100 bps in 2025. The forthcoming rate cuts, coupled with lower bond yields, will bolster commercial real estate investment activity and asset values. CBRE forecasts a 5% increase in annual investment activity this year, with further acceleration next year. Despite slowing job growth, we expect the economy will avoid a recession and a soft landing will buoy occupier confidence, resulting in resilient demand for space across all commercial property types.

|

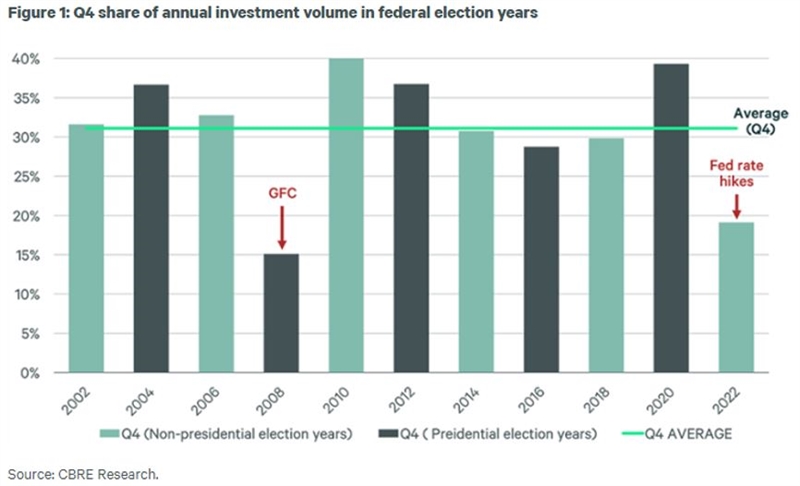

Federal Elections Have Little Immediate Impact on Real Estate Investment Activity

CBRE finds that there has been no material change in commercial real estate investment activity or values in the months just before and after federal elections, despite widespread belief to the contrary. This is not to say that certain policy proposals will not impact commercial real estate market fundamentals and investment activity in the long term. Key policy areas that could impact commercial real estate during the next presidential administration include trade, taxes, regulations, government spending and the federal budget deficit.

|

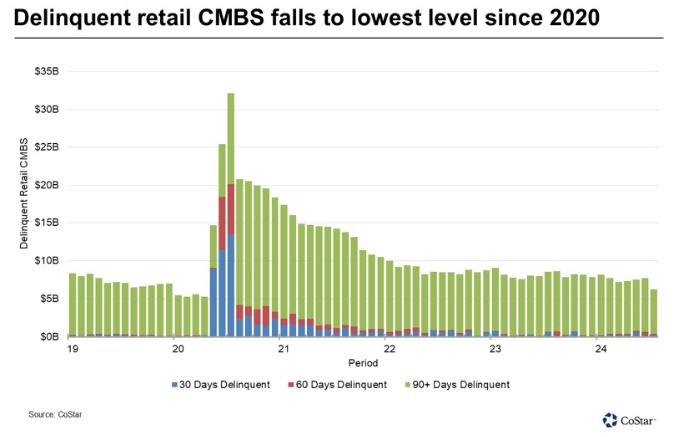

Retail CMBS loans behind on payments recede further

The delinquency rate for retail commercial mortgage-backed securities (CMBS) has decreased to its lowest level since the pandemic, with $6.3 billion in delinquent loans as of July, representing 5.6% of total outstanding CMBS loans. This decline contrasts with trends in the office, hospitality, and multifamily sectors, driven by post-pandemic consumption and favorable market conditions. However, challenges remain, particularly for loans delinquent for over 90 days and properties in maturity default, especially regional and super regional malls. Falling interest rates and a strong retail environment may improve refinancing opportunities by 2025, but some borrowers may still struggle.

|

Despite market sentiment that interest rates are currently elevated, they are still well below the historic long-term average 10-Year US Treasury rate of 5.86% (since 1962). The yield curve for mid-to-long term maturities is no longer inverted indicating investor sentiment that a potential recession is no longer on the near-term horizon. The Federal Reserve has begun an easing cycle, lowering its benchmark rate by 50 basis points, with further cuts anticipated. This reduction in rates presents opportunities for investors, such as refinancing existing loans and expanding portfolios. However, the pace and extent of future rate cuts will depend on economic data and inflation trends. While the Fed aims to balance employment and inflation, there is still a possibility of a recession, which could influence the overall economic landscape and the multifamily market. Credit spreads have compressed since the beginning of the year and there are bridge loan products available providing short term flexibility to those borrowers in need of finding gap funding in anticipation of rates dropping before locking in long-term permanent financing.

We have seen a rise in the number of real estate owners increasing their transaction velocity as they have patiently waited for clarity on timing of rate relief which has already begun to flush through the market as treasury indexes have declined. Those who are facing increased borrowing costs from floating interest rates or near-term maturities of their relatively low fixed rate loans need accretive financing. Investors have capital ready to deploy and many will not wait to be the last to transact before declaring that asset prices and rates are stable.

As active participants in the market across a broad range of lender and product types, our Team is well positioned to identify the most accretive financing solutions, enabling our Clients to consistently achieve the best possible outcomes for their commercial real estate financing needs.

|

|

|

|

|

Unsubscribe

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330). Please consider the environment before printing this email. CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166. Address: 4301 La Jolla Village Drive Suite 3000 Suite 700, San Diego CA 92122

THIS IS A MARKETING COMMUNICATION © 2025 CBRE, Inc. All rights reserved. This information has been obtained from sources believed reliable but has not been verified for accuracy or completeness. CBRE, Inc. makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy, completeness, or reliability of the information contained herein. You should conduct a careful, independent investigation of the property and verify all information. Any reliance on this information is solely at your own risk. CBRE and the CBRE logo are service marks of CBRE, Inc. All other marks displayed on this document are the property of their respective owners, and the use of such logos does not imply any affiliation with or endorsement of CBRE. Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

|

|