|

|

| Slight Increase in Holiday Retail Sales Expected This Year |

Holiday retail sales growth is expected to moderate this year as persistent inflation, lower savings rates, rising credit-card debt and higher interest rates begin to take their toll on consumer confidence.

Read More |

|  |

|

| Food & Beverage Tomorrow: Online grocery order fulfillment goes local |

While most groceries are still sold in stores, just 6.6% of food and drink sales occur online, according to Forrester, and online sales are forecast to grow 12.9% annually through 2028. This may lead to changes in how the grocery industry approaches its retail and industrial real estate strategy.

Read More |

| |

|

| Insurance costs heavily increased in climate sensitive states |

Insurance is comprising a larger share of OPEX nationwide, but the increase is especially acute in states with significant climate change exposure.

Read More |

|

|

|---|

|

|

| Economic Watch: U.S. Labor Market Continues to Cool |

- The U.S. added 150,000 jobs in October, below consensus expectations of 170,000. Job growth totals for August and September were lowered by 62,000 and 39,000, respectively.

- Health care & education (89,000) and government (51,000) accounted for 93% of the jobs added in October.

- Traditional retail gained just 700 jobs in October, while food services & drinking places lost 7,500. Although consumer spending has remained strong, we expect that demand for retail real estate will weaken as the economy slows.

Read More |

| |  |

|

|

|

| |

| Economic Watch: Fed Continues to Hold Rates Steady |

- The Federal Reserve held the federal funds rate at a range of 5.25% to 5.50% today for the second consecutive time. The central bank also affirmed that it will continue to reduce its balance sheet

- Core inflation has been steadily falling over the past 12 months and likely will continue doing so as the economy weakens in Q4.

|

|

|

| |

| What drove Austin’s ascent—and who is poised to follow? |

| A common question in the real estate forecasting business is: what city will be the next Austin? The reality is Austin’s emergence into a top-tier market was decades in the making, supported by the University of Texas, Michael Dell, and maybe even Willie Nelson.

|

|

|

|

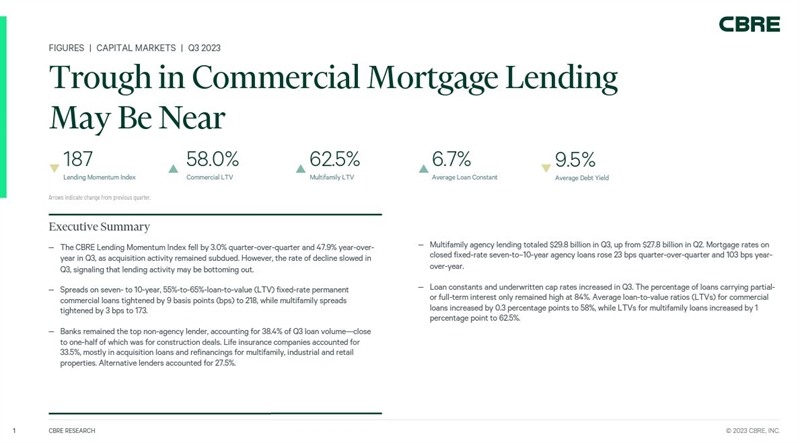

Trough in Commercial Mortgage Lending May Be Near

|

|

|

|

Executive Summary

- The CBRE Lending Momentum Index fell by 3.0% quarter-over-quarter and 47.9% year-over-year in Q3, as acquisition activity remained subdued. However, the rate of decline slowed in Q3, signaling that lending activity may be bottoming out.

- Spreads on seven- to 10-year, 55%-to-65%-loan-to-value (LTV) fixed-rate permanent commercial loans tightened by 9 basis points (bps) to 218, while multifamily spreads tightened by 3 bps to 173.

- Banks remained the top non-agency lender, accounting for 38.4% of Q3 loan volume—close to one-half of which was for construction deals. Life insurance companies accounted for 33.5%, mostly in acquisition loans and refinancings for multifamily, industrial and retail properties. Alternative lenders accounted for 27.5%.

- Multifamily agency lending totaled $29.8 billion in Q3, up from $27.8 billion in Q2. Mortgage rates on closed fixed-rate seven-to–10-year agency loans rose 23 bps quarter-over-quarter and 103 bps year-over-year.

- Loan constants and underwritten cap rates increased in Q3. The percentage of loans carrying partialor full-term interest only remained high at 84%. Average loan-to-value ratios (LTVs) for commercial loans increased by 0.3 percentage points to 58%, while LTVs for multifamily loans increased by 1 percentage point to 62.5%.

|

|

| 10-Year Treasury Yield: Higher for Longer but Not Forever |

The recent bond market sell off has lifted the 10-year Treasury yield to nearly 5% and further dampened investor sentiment for commercial real estate.

Several factors are undermining bond values, but higher inflation is not one of them. Inflation has been falling and is near the Fed’s most recent 10-year expectation of between 2% and 3%.1 Three-month annualized core inflation is close to the Fed’s 2% target.

|

| |  |

|

|

|

|

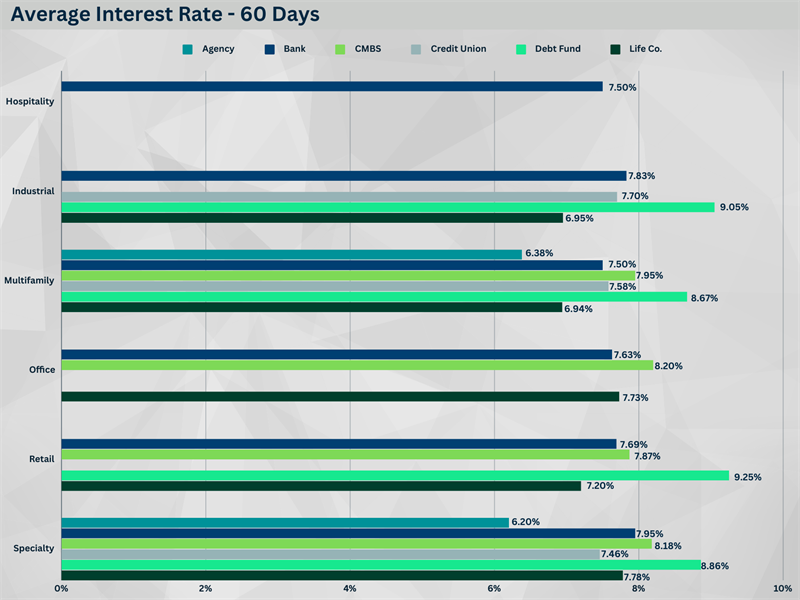

Interest Rate Averages by Lender Type & Asset Type

|

|

|

|

|

Index Rates as of 11/13/2023

|

|

Treasuries

|

Swaps

|

LIBOR

|

|

5-year

|

4.6674%

|

5-year

|

4.661%

|

1-mo

|

5.43739%

|

|

7-year

|

4.6933%

|

7-year

|

4.595%

|

3-mo

|

5.64133%

|

|

10-year

|

4.6365%

|

10-year

|

4.572%

|

6-mo

|

5.8475%

|

|

|

|

|

|

SOFR

|

|

|

|

|

|

1 Mo Avg

|

5.32404%

|

|

|

|

|

|

1 Mo Term

|

5.32291%

|

|

|

|

|

What is a "Buydown"?

Real Estate Terminology Explained

|

|

|

|

A buydown is a mortgage financing technique with which the buyer attempts to obtain a lower interest rate for at least the first few years of the mortgage or possibly its entire life. A 2-1 buydown, for example, is a specific type of mortgage buydown that allows homebuyers to save on their interest rate for the first two years of the loan. Buydowns can also use a 3-2-1 structure as well. | |

|

|

| The 7 Habits of Highly Effective People: 30th Anniversary Edition |

One of the most inspiring and impactful books ever written, The 7 Habits of Highly Effective People has captivated readers for nearly three decades. It has transformed the lives of presidents and CEOs, educators and parents—millions of people of all ages and occupations.

Find Here |

| |

|

| Real Estate Investing Gone Bad: 21 true stories of what NOT to do when investing in real estate and flipping houses |

Discover 21 true stories of real estate investing deals that went terribly wrong and the lessons you can learn from them. The cost of these "deals gone bad" total millions of dollars in losses, years of unproductive activity and incalculable emotional stress. However, you’ll obtain the enormous benefits of the powerful and profitable learning lessons from these 21 mishaps without the costs!

Find Here |

| |

|

| Principles: Life and Work |

Ray Dalio, one of the world’s most successful investors and entrepreneurs, shares the unconventional principles that he’s developed, refined, and used over the past forty years to create unique results in both life and business—and which any person or organization can adopt to help achieve their goals.

Find Here |

|

|

|---|

|

|

Upcoming Events | Connect With Us

|

|

|

|

|

|

The Weekly Take Podcast | CBRE

|

|

|

|

We'd love to discuss financing options with you ! |

|

| Please use the scheduling button to set a meeting with one of our members. |

| |

|

|

|

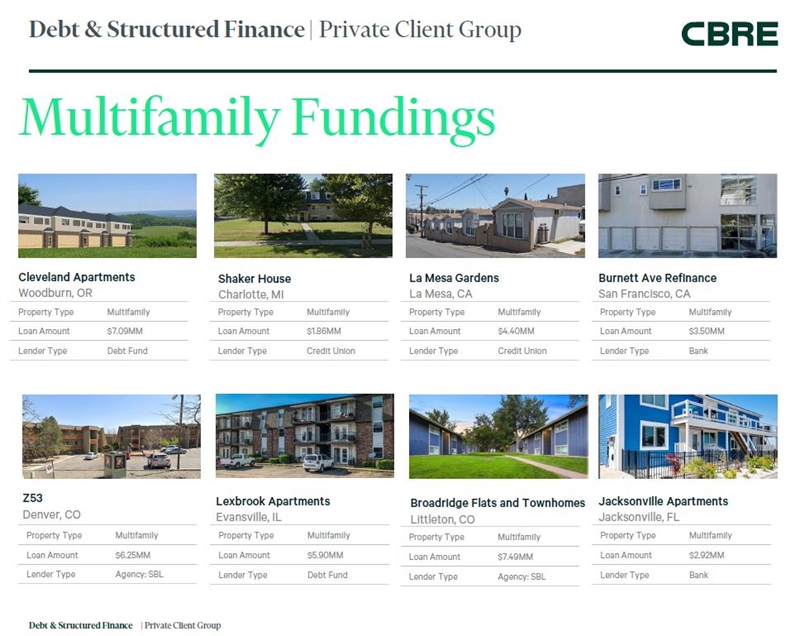

| Our group specializes in debt and structured finance of commercial assets, including multifamily, for private clients nationwide. Located in major markets across the country, including Los Angeles, Phoenix, San Diego, San Jose, and New York our access to market data, investors, and lenders is vast. Each member adds a layer of depth to the overall skill, talent, and expertise of the team. The group’s synergetic endeavors provide a high-level commitment to each deal and the client experience. |

| |

| Click to Download Full Version | |  |

|

|

|

|

|

|

Unsubscribe

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330). Please consider the environment before printing this email. CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166. Address: 2575 East Camelback Road, Suite 500 Suite 700, Phoenix AZ 85016

THIS IS A MARKETING COMMUNICATION © 2026 CBRE, Inc. All rights reserved. This information has been obtained from sources believed reliable but has not been verified for accuracy or completeness. CBRE, Inc. makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy, completeness, or reliability of the information contained herein. You should conduct a careful, independent investigation of the property and verify all information. Any reliance on this information is solely at your own risk. CBRE and the CBRE logo are service marks of CBRE, Inc. All other marks displayed on this document are the property of their respective owners, and the use of such logos does not imply any affiliation with or endorsement of CBRE. Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

|

|

.png)