|

|

We are fortunate to meet daily with a wide array of credible, experienced executives across all industry types and markets. The honest conversations we have and the decisions we make together grant our team with unique insights on what businesses are thinking and doing in real time.

Never has the office market changed so dramatically than over the last two years and our clients' feedback has been invaluable to better understanding what the future holds for their businesses and our industry. The catalyst for this change started with health and safety concerns that prevented offices from being open. However, as the pandemic wanes and we better understand how to effectively live with Covid and combat its negative consequences, we are now faced with new challenges: the changing economy and its effects on the labor market. |

|  |

| Amy Sanchez, Will Hightower and Nicolina Athanas (left to right) at the C-Level @ A Mile High, hosted by the Colorado Technology Association. |

|

|

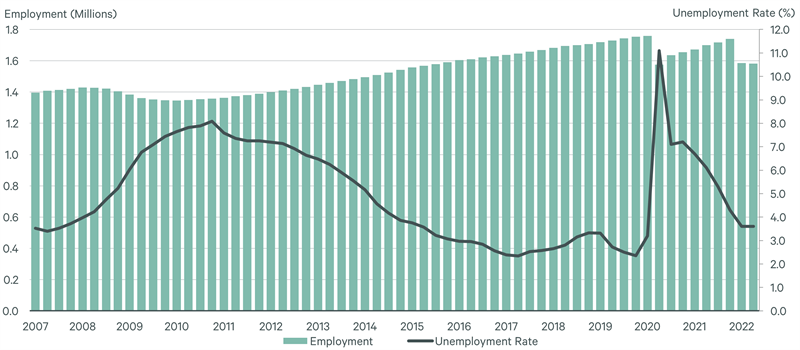

The US unemployment rate is currently at 3.6%, nearing a 50-year low. If you were born before 1985 you may recall a time when landing a job was a feat unto itself. From there, you probably remember working in an office at least 5 days per week, staying late to get ahead, and working your way up the corporate ladder. In a matter of two years, that corporate office culture now seems to be utterly archaic and out of touch. Driven by an imbalance in the labor market, the employee has far more leverage over their working environment than the employer.

Many executives we hear from quietly want their employees to return to the office for the benefits of productivity, innovation & culture. Nevertheless, most are treading carefully knowing that any missteps in pushing back on employee demands could increase attrition and affect retention in a labor market that is still unforgiving but beginning to show signs of weakness.

Although we are experiencing increases in office leasing activity and most companies have initiated a return-to-work policy involving hybrid occupancy strategies, the occupancy rates of office buildings across major metro markets in the US are still much lower than we anticipated at this point. What started out as a health and safety concern for employees has quickly pivoted to a whole host of reasons employees are pushing to work from home such as crime, fuel costs, traffic congestion, and child-care.

This is why many major employers have recently expressed their concerns to local governments and other downtown development organizations alike. “The divide has created a sense of urgency among politicians and business leaders in these cities, where the stakes are especially high because office workers are the engine of local economics and fuel small businesses” ( WSJ, “Big Cities Can’t Get Workers Back to the Office”). These are issues that local governments are acutely aware of as they are struggling with their own return to office policies, knowing that a return is better for their city while simultaneously not wanting to risk the loss of current staff. |

With all the variables in the economy, employers are focused on strong teamwork and efficiencies, which they find occurs better in the office. Our thesis is that a full return to the office will only revert to pre-pandemic levels when the employer gains its position of leverage. How does this occur? We believe that the economy is the impetus for change on the office occupancy front and we are starting to see that transpire as we experience inflationary and recession concerns.

As of June, the CPI rose 9.1% year-over-year, which is the largest gain since 1981. Persistently rising interest rates are putting pressure on corporate borrowing, in addition to labor costs. As inflation continues to rise, we see consumer spending and hiring slow, along with an increase in layoffs. Whether we are currently in or headed for a recession remains to be seen, but the markets are generally pointing towards a shift in the balance of employee/employer relations. US-based companies announced plans to cut 24,286 jobs from their payrolls in April of 2022, the most since May last year.

You may recall Elon Musk’s recent memo to employees rebuking the work from home movement stating that “Remote work is no longer acceptable. Anyone who wishes to do remote work must be in the office for a minimum (and I mean *minimum*) of 40 hours per week or depart Tesla,” and finally capping off his sentiment with “They should pretend to work somewhere else” ( Forbes). Not surprisingly, Elon followed up the next month announcing a 10% reduction in Tesla’s salaried workforce. So, while companies may still be reluctant to take a hard-line approach to their return to office policies as they compete with employers around the world for talent, the labor market is simultaneously shifting below us and the impacts of that fact should not be discounted. |

Elon is not alone in his sentiments. Daniel E. Greenleaf, President and CEO of Modivcare, a healthcare services company based in Colorado in the Southeast Suburban Market, wrote an opinion piece in the Wall Street Journal titled 'Rude Awakening Is Ahead for Young Employees.' Siting a lack of "committed workers" in the U.S., Greenleaf has hired in Bangalore for certain positions, noting a comparable skill set with a much lower turnover rate. As for his U.S. employees, Greenleaf states, "A motivated employee is willing to come into the office. This requirement runs contrary to the post pandemic work-at-home revolt, but it creates the best experience for the patients we serve, boosts team morale, and helps our employees develop professionally."

Not surprisingly, we have become myopic and siloed post-Covid and forget that nature and history repeat itself. We still live in a free-market economy that rewards businesses with the best products and ideas that are executed in the most efficient and productive way. Competition is what drives us forward and shareholders remind us of this every day. This combined with the feedback we receive from each of you tells us that business leaders do want their employees back in the office and perhaps the negative consequences of a slowing economy will be the catalyst for this transition to a new but more recognizable normal. |

| |

| Click here for this must-read article in the WSJ: |

| "A recession will be a rough way to learn this important lesson, but employees and employers will be better for it." - Daniel Greenleaf |

|

|

|

There is no doubt that there are a number of near-term hurdles to overcome for many employers, but one thing we know for certain is that the office is not dead. It's transforming, adapting, and being reimagined - all with the economy in focus.

|

|

|

| 1. LEASING ACTIVITY |

| Quarter-over-quarter, leasing activity declined by 16.8% as tenants continue to evaluate their space requirements and return-to-work strategies. |

|

|

|

|

|

| 2. EMPLOYMENT |

| Office-using employment grew by 4.6%, while professional & business services posted 8.0% job growth and added 25,500 jobs year-to-date. |

|

|

|

|

|

| 3. DEVELOPMENT |

| The office construction pipeline totaled 2.4 million sq. ft. under construction. Seven projects totaling 1.6 million sq. ft. broke ground this quarter across multiple submarkets. |

|

|

|

|

|

| 4. ABSORPTION |

| Year-to-date, 121,000 sq. ft. has been absorbed in Metro Denver, significant improvement from the negative 1.8 million sq. ft. in Q1 & Q2 2021. |

|

|

|

|

|

| 5. INVESTMENT |

| The most notable sale this quarter based on price was Flatiron Park, a 1.0 million sq. ft. office and life sciences campus in Boulder that sold for $538.54 psf. |

|

|

|

|---|

|

Our Client Success Stories |

|

| Gen II |

|

Serving as the company's new western headquarters, this 72,000 SF office is situated in one of the best new construction assets in the Southeast Suburban market. Belleview Station has evolved and continues to add Class A office space, top tier living options, and a diverse set of high quality retail businesses.

|

| |

|

| Walker & Dunlop |

|

In the very competitive Cherry Creek North micro-market, we were able to secure one of the largest new leases in the market for our client while obtaining favorable terms. This financial firm will settle into 26,861 SF of new construction in Q4 2023. The Class A building, 300 University Blvd, started construction in May of 2022 and will deliver with the office 100% leased.

|

| |

|

| Undisclosed (North Dakota) |

|

This was a complex project which took 3 years to optimally position the client and fully complete. The sale of this property in Dickinson, ND involved several parties and transactions to maximize the net proceeds to our client. It was a fun project, with plenty of creative solutioning in a market that is very dependent on macro-level economic factors.

|

|

|

|---|

|

|

Click below to view the CBRE Q2 2022 Marketview Office Reports:

|

|

Related news...

|

|

|

ZUCK TURNS UP THE HEAT

As Meta's growth slows, Mark Zuckerberg is pushing even harder. Will his employees melt under the pressure?

READ MORE |

| |

|

|

A wave of layoffs is sweeping the US. Here are firms that have announced cuts so far, from Coinbase to Tesla.

READ MORE |

| |

|

|

Despite Strengthening Headwinds, Global Economy May Still Avoid Recession

READ MORE |

|

|

|---|

|

|

|

Featuring the Albanese/Weld Team...

|

|

|

Panelist: Anthony Albanese

2022 Office End-User Conference will be held in-person the morning of Monday, August 29, 2022 at the Hyatt Regency Aurora-Denver Conference Center.

REGISTER NOW |

| |

|

|

Oil's presence in downtown Denver shrinks despite price boom

READ MORE |

|

|

|---|

|

|

|

|

|

|

Unsubscribe

You may also unsubscribe by calling toll-free +1 877 CBRE 330 (+1 877 227 3330). Please consider the environment before printing this email. CBRE respects your privacy. A copy of our Privacy Policy is available online. For California Residents, our California Privacy Notice is available here. If you have questions or concerns about our compliance with this policy, please email PrivacyAdministrator@cbre.com or write to Attn: Marketing Department, Privacy Administrator, CBRE, 200 Park Ave. 19-22 Floors, New York, NY 10166. Address: 1225 17th Street Suite 3200, Denver CO 80202

THIS IS A MARKETING COMMUNICATION © 2026 CBRE, Inc. All rights reserved. This information has been obtained from sources believed reliable but has not been verified for accuracy or completeness. CBRE, Inc. makes no guarantee, representation or warranty and accepts no responsibility or liability as to the accuracy, completeness, or reliability of the information contained herein. You should conduct a careful, independent investigation of the property and verify all information. Any reliance on this information is solely at your own risk. CBRE and the CBRE logo are service marks of CBRE, Inc. All other marks displayed on this document are the property of their respective owners, and the use of such logos does not imply any affiliation with or endorsement of CBRE. Photos herein are the property of their respective owners. Use of these images without the express written consent of the owner is prohibited.

|

|

|